For some, Finance is intriguing; you want to learn all you can to set yourself up in the best possible position – “Financial Independence”. For others, it’s very confusing. Whether you know nothing about finance, or feel highly knowledgeable and just want the hottest stock tip, my goal in this series is to help readers gain some financial knowledge that will help to achieve your goals.

Financial knowledge is a vast area, with individual needs varying widely depending on personal situations and competencies. Learning about Finance can be frustrating, but if you stick with me I’ll teach you how to eliminate frustration and empower you with the financial knowledge you need to meet your goals – whether it is the near term goal of paying the bills, to save a few bucks for your future, or the ultimate goal of reaching Financial Independence.

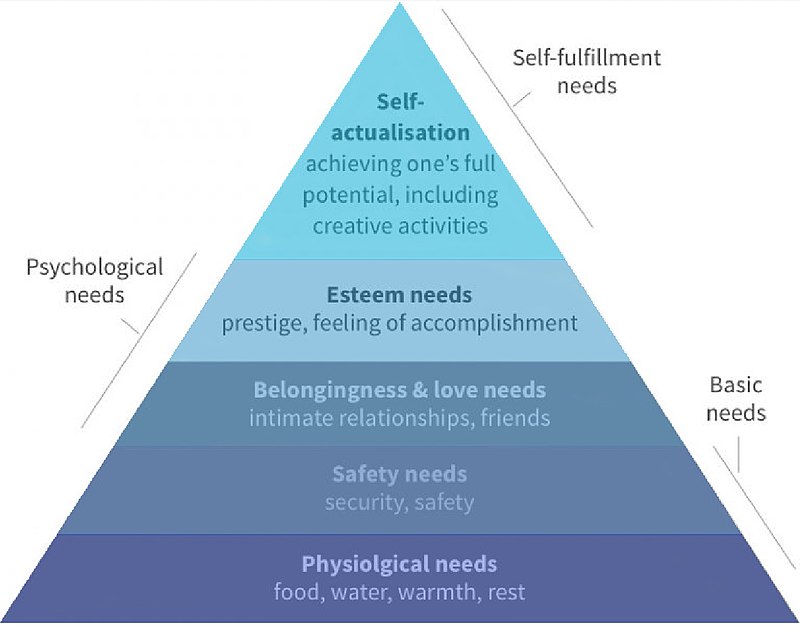

Most of the frustrations around finance are caused by the decisions that you need to make along the way. Financial goals or financial stages in one’s life are like Maslow’s Hierarchy of Needs. They are similar in that you need to understand and have control of one stage before you can really move on to the next. Maslow’s Hierarchy of Needs should also remind us that money is only a means to an end. The end isn’t counted in dollars, but in the needs that Maslow laid out years ago. In today’s society however, nearly everything is transacted through money, so in financial terms those stages would look like this:

Maslow’s Hierarchy of Needs

- Physiological Needs = Income for Food, Housing, Utilities

- Safety Needs = Insurance, Savings Account

- Love & Belonging = Disposable Income for Entertainment, Socializing & Credit

- Esteem = College Expenses, Investments, Retirement Accounts

- Self-Actualization = Financial Independence, Philanthropy

TM’s Finance Principle #1 – You are a business called You!

Whether or not you ever wanted to be in business, you and your personal finances are just like any business and their finances. You sell your services to an employer for wages and benefits. At any time they can stop buying or you can stop selling. Your first goal, just like any business, should be to sell a quality product (your services) at a price to cover your overhead (living expenses) and make a profit (your savings). Of course, Uncle Sam takes taxes from profits (your income taxes), but you should have enough left for capital expenditures (investing for your future, your home, your personal growth) and what is left is your Free Cash Flow (your disposable income for entertainment, etc.).

Your second goal, just like a business, is to maximize sales and profit margins (by improving your value through experience and education, and or reducing expenses) to increase your Free Cash Flow (to save and invest to diversify your income streams).

Your third goal, just like a business, is to create a Cash Cow – a brand that keeps bringing in the cash automatically with less marketing (these are investments that you have saved for from your profits/income that should now be earning dividends and interest to make you financially independent, so that you can stop selling your services, if you want to).

Both businesses and people can be successful and thrive, or flounder and fail. Your personal finances are a business called “You” and it is up to you to understand it and manage it.

If you don’t, it will manage you.

A Thought to Consider

Financial Independence can provide you with the time to enjoy more of the things that you want in life whether its golf, gardening, laying on a beach or spending more time with your friends and family. Some people will tell you that “Money isn’t everything; it is the only thing!” I will tell you that money is only a means to an end.

The great Stephen Covey, author of many books including “The 7 Habits of Highly Effective People” told us that one of those habits was to “Begin with the End in Mind”. I would ask you to define your financial goals by what you need to be happy in your life. Everybody doesn’t need a million dollars in the bank to be happy. Many millionaires live unhappy lives and go broke because they can’t manage their personal finances. So, think about your financials goals, write them down, and then we can find the financial means to make them happen.

My Hottest Stock Tip Today Is …

Don’t bet on hot stock tips that you get from friends on the street! Although I’ve done very well in the market, it is not from hot stock tips and it almost never fails that when someone gives me a hot stock tip, I’ve lost money. The only real hot stock tips come from inside information, and insider information is illegal to use and to share with others. People do go to jail for this. If you would like to read a case story just Google Martha Stewart and Insider Trading – she served time related to insider trading charges.

I am often asked for hot stock tips and, although I never give out “hot stock tips”, I may share one or more stocks that I like at the time, but always with caution and a warning. The warning is generally reminding that person that the individual stock may or may not be a good fit for their portfolio.

Every time I buy a stock there is a great amount of analysis that is behind it; I evaluate the company, the current price level of the stock relative to my valuation of the company and its peers, the current market conditions, and how it fits into the portfolio. Once I own a stock, although my intention is generally to hold it for a long-term, my analysis is an ongoing process that eventually leads to a decision to buy more, continue to hold it, or sell some or all of it.

Featured in Forbes for his portfolio’s 28% avg. return over 10 years, Tony Mitchell uses his business experience and MBA, MS/Finance and BBA/Marketing education to continue to outperform the averages at Marketocracy.com

Visit Tony Mitchell at apmitchell.mytrackrecord.com